How to File Business Taxes for an LLC (2026 Tax Year Guide)

Filing LLC taxes isn't a one-size-fits-all process. Your structure determines which IRS forms you file and whether you owe self-employment tax.

Over 6 years of consulting, I've helped more than 40 LLC owners work through tax classification decisions. In 3 of those cases, a missed S corp election deadline meant an unexpected 15.3% self-employment tax bill that could have been avoided entirely.

This guide covers every major LLC tax type, including single-member, multi-member, C corp and S corp. You'll also see the exact forms and deadlines for the 2025 tax year filed in 2026. Aran Quinn, a CPA, Esq., LL.M certified public accountant and tax attorney at Quinn Global Tax Law PC, reviewed the guide for accuracy.

Quick Summary

- Filing depends on your LLC's tax classification. Single-member files Schedule C by April 15, 2026. Multi-member files Form 1065 by March 16, 2026. C corp election uses Form 1120 by April 15, 2026. S corp election uses Form 1120-S by March 16, 2026.

- LLCs are taxed by default based on their structure. Single-member LLCs count as disregarded entities and multi-member LLCs count as partnerships. To elect corporate taxation, file IRS Form 8832 or Form 2553 for S-corp status.

- LLCs electing S Corp taxation can reduce the 15.3% self-employment tax by allocating income between a reasonable salary and distributions, lowering the share exposed to SE tax.

How LLC taxes work — quick overview

By default, the IRS doesn't tax an LLC as its own entity. Instead, the IRS assigns one of three classifications based on how many members you have or which election you file.

- One member. Disregarded entity, so income flows to your personal return on Schedule C.

- Two or more members. Partnership, so the LLC files Form 1065 and issues each member a Schedule K-1.

- Elected corporate treatment. The LLC files Form 8832 for C corp or Form 2553 for S corp and submits its own corporate return.

Three forms drive nearly every decision below. They are Form 8832 for default-classification changes, Form 2553 for the S-corp election and Form 1040 Schedule SE for self-employment tax. Memorize those, and most of the filing logic follows.

State-by-state LLC Tax Requirements

The table below summarizes how each state taxes LLCs. Click any state for a full breakdown of forms, deadlines and franchise fees specific to that state.

| State | Personal income tax | LLC franchise/fee | Notes |

| Alabama | Yes (up to 5%) | BPT $100 min (exempt if ≤$100) | Separate annual report eliminated for 2024+ |

| Alaska | No personal income tax | $100 biennial report | Individual income tax repealed; corporate income tax applies if C-corp elected |

| Arizona | Yes (2.5% flat) | None | No annual report or franchise tax |

| Arkansas | Yes (up to 3.9%) | $150/year | Annual franchise tax report due May 1 |

| California | Yes (up to 13.3%) | $800/year min | Plus $20 biennial SOS statement (LLC-12); gross-receipts fee if >$250K revenue |

| Colorado | Yes (4.4% flat) | $25/year periodic report | Fee increased from $10 to $25 effective July 1, 2024 |

| Connecticut | Yes (up to 6.99%) | $80/year annual report | Annual report due March 31; Business Entity Tax repealed 2020 |

| Delaware | Yes (up to 6.6%) | $300/year flat | Due June 1; owed even with no DE operations |

| Florida | No personal income tax | $138.75/year annual report | Due May 1; $400 late penalty after May 1 |

| Georgia | Yes (5.19% flat) | $60/year annual registration | Due April 1; fee is $50 + $10 service charge (eff. Sept 2025) |

| Hawaii | Yes (up to 11%) | $15/year annual report | General excise tax (4%) on gross receipts also applies |

| Idaho | Yes (5.3% flat) | $0 annual report (free online) | Rate cut from 5.695% eff. Jan 2025; annual report due annually |

| Illinois | Yes (4.95% flat) | $75/year annual report | Personal property replacement tax (1.5%) may also apply |

| Indiana | Yes (2.95% flat) | $32 biennial report | Rate scheduled to drop to 2.9% in 2027; report due every 2 years |

| Iowa | Yes (3.8% flat) | $30 biennial report | Flat rate took effect Jan 2026 (was bracketed up to 5.7%); biennial due in odd years |

| Kansas | Yes (up to 5.58%) | $90/year information report | Biennial report due April 15; 5.20%/5.58% two-bracket structure |

| Kentucky | Yes (3.5% flat) | $175/year min LLET | Plus $15/year annual report (SOS); LLET min applies even under $3M gross |

| Louisiana | Yes (3% flat) | $25/year annual report | Flat rate effective Jan 2025 (was graduated up to 4.25%); franchise tax for corps only |

| Maine | Yes (up to 7.15%) | $85/year annual report | Annual report due June 1; 9.15% surcharge on income over $1M |

| Maryland | Yes (up to 6.5%) | $300/year annual report | New 6.25%/6.5% brackets eff. TY2025; plus local income tax (up to 3.3%) |

| Massachusetts | Yes (5% flat) | $500/year annual statement | 4% surtax on income over $1,107,750 (2026 threshold); due on LLC anniversary date |

| Michigan | Yes (4.25% flat) | $25/year annual statement | Annual statement due Feb 15; $50 late penalty |

| Minnesota | Yes (up to 9.85%) | $0 annual renewal | Free annual renewal; 9.85% kicks in above $203,150 (single, 2026) |

| Mississippi | Yes (4% flat) | $0 annual report | 4% on income over $10K (TY2026, down from 4.4% in TY2025); phaseout to 0% planned |

| Missouri | Yes (up to 4.7%) | No annual report | No franchise tax; no recurring LLC fee |

| Montana | Yes (up to 5.65%) | $0/year annual report | No sales tax; $35 late fee if after Apr 15; rate reduced from 5.9% in 2026 |

| Nebraska | Yes (up to 4.60%) | $30 biennial report | Biennial report due Apr 1 in odd years; rate reduced under LB 754 |

| Nevada | No personal income tax | $350/year ($150 list + $200 license) | Commerce tax applies if gross revenue >$4M |

| New Hampshire | No personal income tax | $100/year annual report | I&D tax repealed Jan 2025; BPT/BET on business profits |

| New Jersey | Yes (up to 10.75%) | $75/year annual report | Partnership filing fee $150/partner (capped $250K) |

| New Mexico | Yes (up to 5.9%) | None | No annual report required; no franchise tax for LLCs |

| New York | Yes (up to 10.9%) | $25–$4,500/year | Annual LLC filing fee based on NY-source gross income |

| North Carolina | Yes (3.99% flat) | $200/year annual report | Flat rate reduced from 4.25% (2025) to 3.99% (2026+) |

| North Dakota | Yes (up to 2.50%) | $50/year annual report | Rates range 1.10%–2.50%; report due Nov 15 |

| Ohio | Yes (2.75% flat) | None | No annual report; CAT applies on gross receipts over $150K |

| Oklahoma | Yes (up to 4.5%) | $25/year annual certificate | Rate reduced from 4.75% to 4.5% for TY2026 per HB 2764 |

| Oregon | Yes (up to 9.9%) | $100/year annual report | No state sales tax; 9.9% applies above $125K (single) |

| Pennsylvania | Yes (3.07% flat) | $7/year annual report | Annual report due Sept 30; local EIT may also apply |

| Rhode Island | Yes (up to 5.99%) | $400/year minimum annual charge | Plus $50 SOS annual report; $400 minimum tax regardless of profit |

| South Carolina | Yes (up to 5.21%) | None | Rate reduced from 6.2% to 5.21% (TY2026) per H. 4216; no annual report for pass-through LLCs |

| South Dakota | No personal income tax | $55/year annual report | No income tax or franchise tax; one of 7 no-income-tax states |

| Tennessee | No personal income tax | $300/year annual report | Hall tax repealed Jan 2021; F&E tax: 6.5% excise on net earnings + $100 min franchise |

| Texas | No personal income tax | Franchise tax if revenue >$2.65M | No annual report; PIR required; 0.75% rate on taxable margin |

| Utah | Yes (4.5% flat) | $18/year annual report | Flat rate reduced from 4.55% to 4.5% starting TY2025 |

| Vermont | Yes (up to 8.75%) | $45/year annual report | Four brackets 3.35%–8.75%; fee updated from $35 per 11 V.S.A. § 4012(a)(15) |

| Virginia | Yes (up to 5.75%) | $50/year annual registration | Fee due July 1, payable by Sept 30; 5.75% applies above $17K |

| Washington | No personal income tax | $70/year annual report | B&O tax on gross receipts also applies; one of 7 no-income-tax states |

| West Virginia | Yes (up to 4.58%) | $25/year annual report | Rate cut to 4.58% for TY2026 per SB 392 (signed March 31, 2026) |

| Wisconsin | Yes (up to 7.65%) | $25/year annual report | $40 if filed by mail; deadline based on formation-anniversary quarter |

| Wyoming | No personal income tax | $60 min/year annual report | Fee scales with WY assets ($0.0002×assets); one of 7 no-income-tax states |

State tax data changes frequently. Confirm current rates with your state department of revenue before filing.

LLC tax filing deadlines for 2025 tax year

| Form | Who files | Due date |

| Schedule C (Form 1040) | Single-member LLCs | April 15, 2026 |

| Schedule SE (Form 1040) | Any LLC member with ≥$400 net SE earnings | April 15, 2026 |

| Form 1065 + Schedule K-1 | Multi-member LLCs (partnership) | March 16, 2026 |

| Form 1120-S + Schedule K-1 | LLCs taxed as S corp | March 16, 2026 |

| Form 1120 | LLCs taxed as C corp | April 15, 2026 |

| Form 2553 | LLCs electing S-corp status for 2026 | March 16, 2026 (75 days from year start) |

| Form 8832 | LLCs changing entity classification | Effective date ±75 days |

| Form 1040-ES (Q1 estimate) | All LLC members owing >$1,000 fed tax | April 15, 2026 |

Filing taxes by LLC type

Start by identifying your LLC's tax classification. That's what drives everything else. The default classification is set by member count. Corporate treatment requires an explicit election with Form 8832 or Form 2553.

If you're a first-time filer, go through a checklist before you do anything. Pay extra attention if you need Forming LLC Without SSN. Keep in mind that state tax requirements vary depending on where your business is registered.

From there, determine What Tax Form Does Your LLC File. If you're unsure which applies, a tax professional can help you sort it out quickly.

Let's get into more detail about how LLC owners pay taxes, and first let’s learn What are the Different Types of LLC.

Single-member LLC (disregarded entity)

If your LLC had little or no revenue this year, start with our guide on How to File Taxes for an LLC With No Income. The rules are different from a profitable single-member LLC.

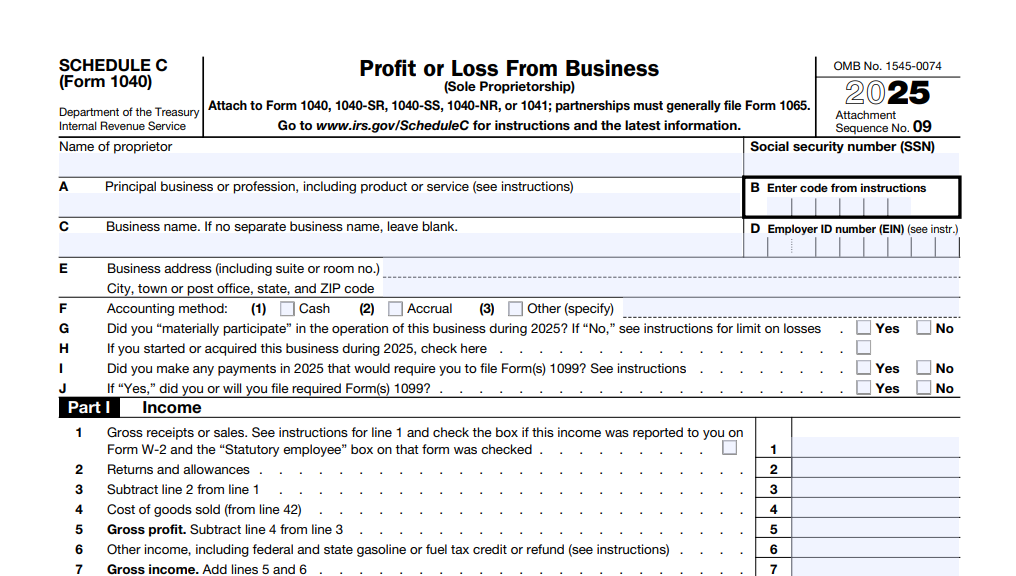

As a single-member LLC, the IRS taxes you like a sole proprietorship. All income flows directly to you as the owner, and you report any profit, expense or loss on your personal tax return.

In practice, that means filing Schedule C (Form 1040) by April 15, 2026 for the 2025 tax year. It's one of the simpler filings you'll deal with, but don't confuse "simple" with "optional."

For tax purposes, a single-member LLC is also called a disregarded entity. That's IRS language for "we're treating this like you and the business are the same thing."

You'll also file Schedule SE (Form 1040) to calculate self-employment tax at 15.3% on net earnings of $400 or more. Schedule SE is filed alongside your Schedule C with your personal return.

If your state has an income tax, you'll also file a state personal income tax return reporting the LLC income. Rates and deadlines vary by state, so see the state-by-state table below.

If you’re considering How to Avoid & Reduce Self Employment Tax, think about electing corporate taxation for the disregarded entity.

You will also have to complete an Internal Revenue Service Schedule C as a single-member LLC owner, which is the same form sole proprietors use when filing their taxes.

If you want to minimize your self-employment tax burden, opt for electing corporate taxation for the disregarded entity.

Multi-member LLC (partnership)

LLCs with two or more members are taxed like partnerships by default. Income flows directly to each member, so there's no entity-level tax.

With multiple-member LLCs, here's how the filing process actually works.

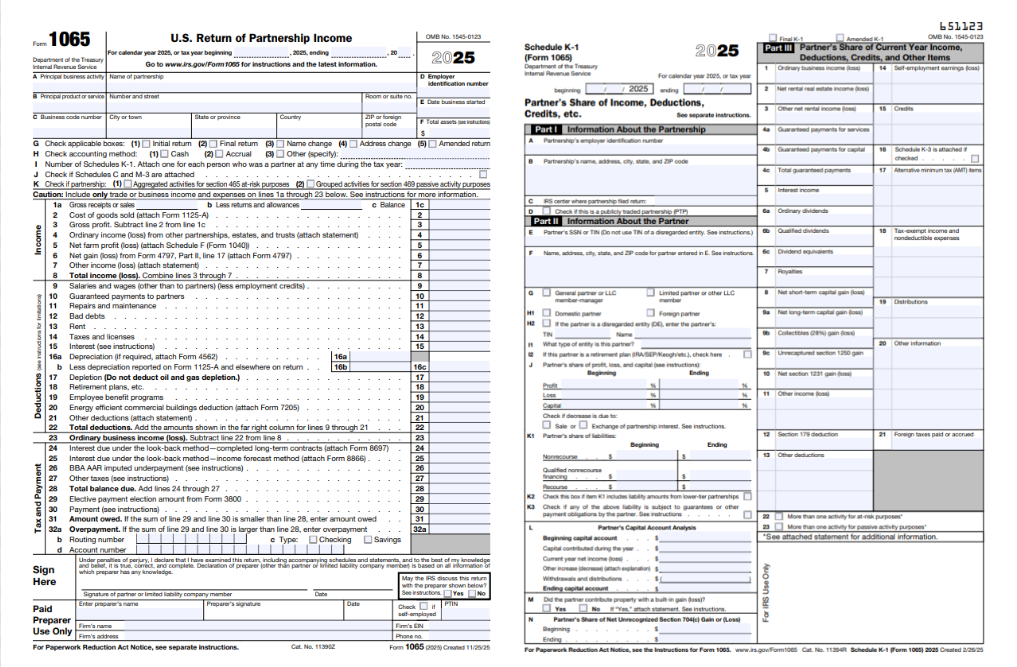

- The LLC reports all income and expenses on IRS Form 1065 (U.S. Return of Partnership Income).

- The LLC then issues a Schedule K-1 to each member, showing that member's share of partnership income, losses, deductions and credits. Before you calculate each K-1, learn How to Split Ownership in an LLC.

- Each member uses the information from their K-1 to report their share of profit or loss on Schedule E (Form 1040) of their personal return.

For the 2025 tax year, Form 1065 is due March 16, 2026 (March 15 falls on a Sunday). Each member's personal Form 1040, including Schedule E, is due April 15, 2026 [1].

Schedule K-1 is issued BY the LLC TO each member. It's not a return the member files themselves. The member uses the K-1 data when preparing their own Form 1040 and Schedule E.

LLC taxed as S corporation

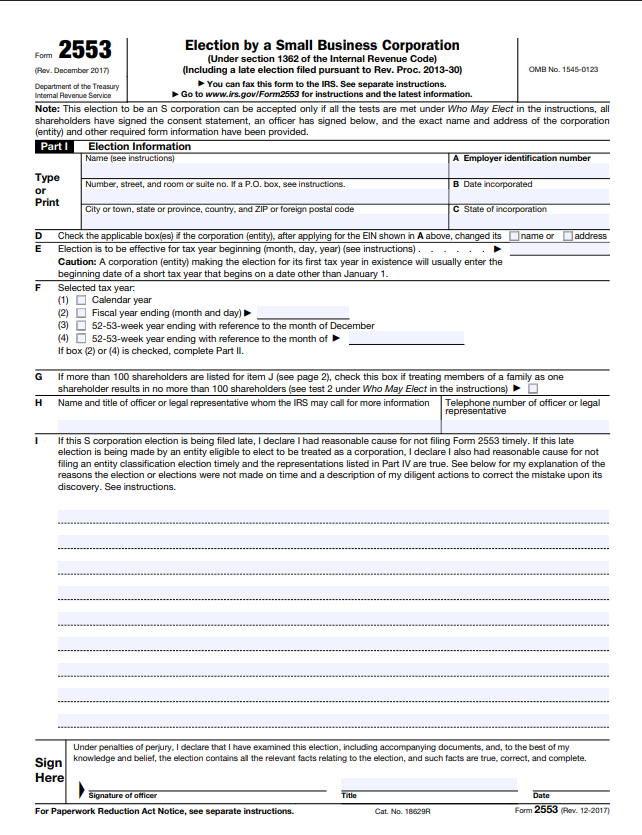

An LLC Electing To Be Taxed As an S Corp must file IRS Form 2553 (Election by a Small Business Corporation) [2]. Electing S-corp status keeps the LLC a pass-through entity while letting owner-members split compensation between salary and distributions.

The LLC then files Form 1120-S with the IRS to report business income and losses [3], and issues a Schedule K-1 to each member. Members report their share on Schedule E of their personal Form 1040.

Deadline. Form 1120-S is due March 16, 2026 because March 15 is a Sunday. Members' personal Form 1040 is due April 15, 2026.

Key compliance rules for S-corp LLCs.

- Reasonable salary requirement. The IRS requires owner-employees of S corps to pay themselves a "reasonable salary" subject to payroll taxes before taking distributions. Paying yourself only distributions to dodge employment taxes is a primary audit trigger. What counts as "reasonable" depends on industry, role and revenue. When in doubt, benchmark against comparable W-2 roles.

- 75-day election window. Form 2553 must be filed within 75 days of the start of the tax year you want it to apply (or within 75 days of formation for new entities). Miss it, and your election doesn't take effect until the following year.

- Eligibility restrictions. S corps are limited to 100 shareholders, must have only U.S. resident shareholders (no foreign members) and can issue only one class of stock. An LLC with any foreign member can't elect S-corp status.

LLC taxed as C corporation

An LLC can elect to be taxed as a C corporation by filing IRS Form 8832 (Entity Classification Election) [4]. Once classified as a C corp, the LLC files corporate income taxes separately from its members' personal returns.

The LLC files Form 1120 (U.S. Corporation Income Tax Return). For calendar-year corporations, Form 1120 is due April 15, 2026 for the 2025 tax year.

The catch is double taxation. Electing C-corp treatment creates two layers of tax.

- The C corp pays corporate income tax (currently 21% federal flat rate) on its profits.

- When the corporation distributes those after-tax profits to members as dividends, the members pay personal income tax on the dividends too.

This is the single most important fact to weigh before electing C-corp status. It can still make sense in a few cases. For example, you might plan to retain earnings inside the business, qualify for the Section 1202 small-business stock exclusion or want corporate-level fringe benefits. Most small LLCs will still pay more total tax under C-corp treatment than under the default pass-through.

I'd recommend talking through the S corp vs. C corp question with a tax professional before you file. The right answer depends on your income level, how you plan to pay yourself and your long-term plans for the business.

Other LLC taxes you need to know

Beyond income tax, most LLCs owe at least one more form of tax. The list covers self-employment tax, estimated quarterly taxes, state income tax, franchise tax or sales tax.

Self-employment tax (15.3%)

LLC members don't get a pass on self-employment tax. Because a default-classified LLC isn't taxed at the entity level, members pay 15.3% on their share of profits. That breaks down to 12.4% for Social Security on earnings up to $176,100 in 2025 and 2.9% for Medicare, which has no earnings cap [5].

There's an additional 0.9% Medicare surtax on self-employment income above $200,000 (single filers) or $250,000 (married filing jointly). It's not part of the standard 15.3% rate but applies on top of it for high earners.

As a pass-through entity, you report your share of profits on your personal return and pay the corresponding taxes there.

This catches a lot of people off guard. I've seen it trip up LLC members who earn music business income from performances, streaming or royalties and didn't realize their entire net share was subject to SE tax.

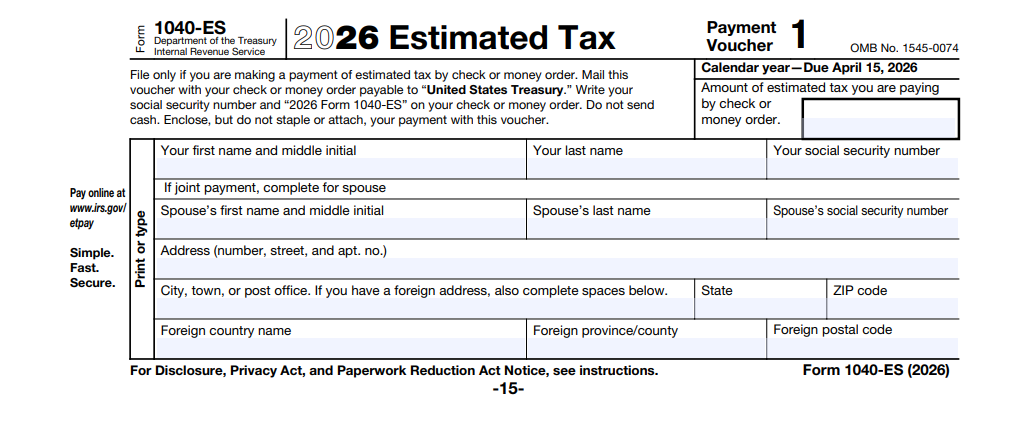

Estimated Quarterly Tax Payments

If you expect to owe more than $1,000 in federal taxes on your LLC income, you must make quarterly estimated tax payments. Use Form 1040-ES (Estimated Tax for Individuals) to calculate and submit them.

The threshold is on federal tax owed, not gross profit, so a high-deduction LLC with low net income may not need quarterly payments at all.

Here are the 2026 quarterly deadlines for 2026 tax-year income.

| Quarter | Income period | Payment due |

| Q1 | January 1 – March 31, 2026 | April 15, 2026 |

| Q2 | April 1 – May 31, 2026 | June 15, 2026 |

| Q3 | June 1 – August 31, 2026 | September 15, 2026 |

| Q4 | September 1 – December 31, 2026 | January 15, 2027 |

Those payments get credited against your annual tax bill, so you're not paying twice. You're just paying earlier.

State income taxes

State income tax is the biggest variable in LLC tax planning. Nine states levy no broad personal income tax at all. California sits at the other extreme with a top rate of 13.3%. See the state-by-state table below for specifics on your state.

Franchise taxes

Many states charge a separate franchise tax (sometimes called an "annual report fee," "LLC tax" or "business privilege tax") just for the privilege of operating as an LLC in that state, separate from income tax. Here are a few examples.

- California charges an $800 minimum annual franchise tax for every LLC, regardless of income.

- Delaware levies a $300 flat annual franchise tax, owed even if your LLC doesn't operate there.

- Texas only applies its franchise (margin) tax if annual revenue exceeds the no-tax-due threshold of $2.47 million for 2024 reports.

- New York charges an annual LLC filing fee that ranges from $25 to $4,500 based on gross income.

- Tennessee charges a franchise and excise tax of $100 minimum, plus 6.5% on apportioned net earnings.

Franchise taxes are often forgotten because they're invoiced separately from federal returns. Missing them is one of the most common ways LLCs fall out of good standing with their state.

Sales tax

If your LLC sells physical products, certain digital goods or some types of services, you'll likely need to collect and remit sales tax to every state where you have economic nexus.

Post-Wayfair (2018), most states impose nexus once you cross either a sales-dollar threshold (commonly $100,000) or transaction-count threshold (commonly 200 transactions), even with no physical presence.

Sales tax is administered by the state department of revenue, not the IRS. Registration, filing frequency and rates vary by state and in some cases by county or city.

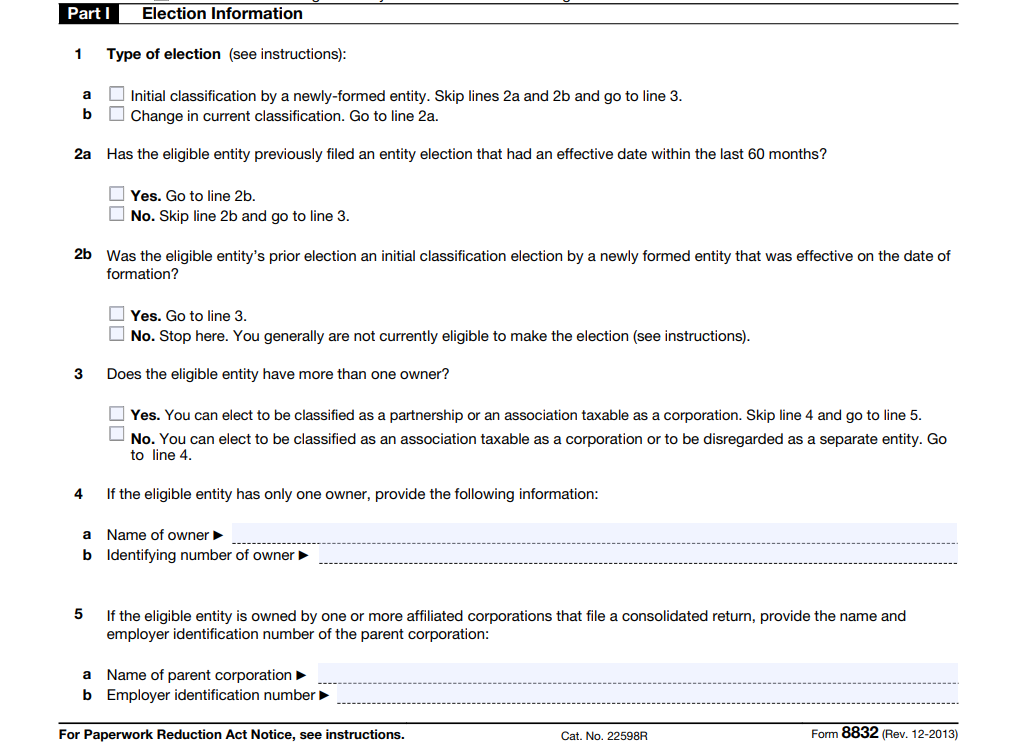

How to change your LLC tax classification

To change your tax classification, file IRS Form 8832 (Entity Classification Election) [4].

By default, the IRS classifies your LLC based on how it's organized and taxes it accordingly. But if you've outgrown that default, or you elected the wrong structure early on, Form 8832 lets you make the switch.

An LLC already classified as a corporation can use this to choose between C corp or S corp treatment.

Once you change your tax classification, you generally cannot change it again for 60 months (5 years). Consider this carefully before electing. A reactive classification change after a single bad tax year can lock you into the wrong structure through several growth stages.

To elect S corp status for the current tax year, file Form 2553 within 75 days of your tax year starting. For calendar-year LLCs, that's the March 16 window. New LLCs follow the same 75-day rule from their formation date, which can be any date in the year.

Miss the window and your election doesn't apply until the following tax year. I've had clients find this out in April when there was nothing left to do about it.

If you do miss it, the IRS allows late S-corp election relief under Revenue Procedure 2013-30 [6], but you must demonstrate reasonable cause for the delay. Don't count on it as a backup plan. Proving "reasonable cause" is harder than most people expect.

FAQs

Is LLC taxed quarterly?

LLCs must make quarterly estimated tax payments if the owner expects to owe more than $1,000 in federal income tax for the year. Payments are made on Form 1040-ES and are due April 15, June 15, September 15 and January 15 of the following year.

What can I write off with an LLC?

You can deduct ordinary and necessary business expenses, including office supplies, equipment, software subscriptions, business travel and mileage, marketing costs, professional services like legal and accounting, business insurance and a portion of home-office expenses if you have a dedicated workspace. You can also deduct half of your self-employment tax on your personal return. Personal expenses are generally not deductible. Home-mortgage interest and property taxes go on Schedule A of your personal return, not as a business expense.

Does LLC pay federal income tax?

LLC does not pay federal income tax by default. An LLC is a pass-through entity, and members pay personal income tax on their share of profits. If the LLC elects C-corp taxation via Form 8832, it does pay federal corporate income tax (currently 21%), and members then pay personal income tax on dividends. That creates the double-taxation scenario described above.

When are LLC taxes due for the 2025 tax year?

The LLC tax due dates for the 2025 tax year vary by entity type. Partnerships (Form 1065) and S corporations (Form 1120-S) are due March 16, 2026. Single-member LLCs (Schedule C), C corporations (Form 1120), and first-quarter estimated payments (Form 1040-ES) are due April 15, 2026.

Do I need to file LLC taxes if my LLC made no money?

Whether you need to file LLC taxes if you LLC made no money depends on your classification. Multi-member LLCs and corporations must file even with zero income. Single-member LLCs generally don't need to file Schedule C with no income or expenses, but most states still require an annual report or fee regardless. When in doubt, file.

What happens if I miss the LLC tax filing deadline?

If you miss the LLC tax filing deadline, penalties depend on which form you missed. Form 1065 and Form 1120-S each carry $235 per partner or shareholder per month, up to 12 months. Form 1120 and Form 1040 carry 5% of unpaid tax per month, up to 25%, plus interest, with separate failure-to-pay penalties of 0.5% per month.

Can I file LLC taxes myself or do I need a CPA?

Single-member LLCs with straightforward income can usually self-file using consumer tax software such as TurboTax Self-Employed, H&R Block, or FreeTaxUSA. Multi-member LLCs, S corps, and C corps are more complex - Form 1065, 1120-S, and 1120 mistakes can trigger entity-level penalties that exceed a CPA's fee.

References:

- https://turbotax.intuit.com/tax-tips/small-business-taxes/business-tax-deadline-guide-for-2024/c6DlyOhp5

- https://www.irs.gov/businesses/small-businesses-self-employed/self-employment-tax-social-security-and-medicare-taxes

- https://www.irs.gov/forms-pubs/about-form-8832

- https://www.irs.gov/pub/irs-pdf/i1065.pdf

- https://www.irs.gov/instructions/i1120s

- https://www.irs.gov/pub/irs-pdf/f2553.pdf

- https://www.irs.gov/pub/irs-drop/rp-13-30.pdf

Heya! I’m at work surfing around your blog from my new iphone 4! Just wanted to say I love reading your blog and look forward to all your posts! Carry on the superb work!

magnificent post, very informative. I wonder why the other experts of this sector do not realize this. You should proceed your writing. I’m sure, you’ve a huge readers’ base already!

I like the helpful information you provide in your articles. I will bookmark your weblog and check again here regularly. I’m quite certain I?ll learn a lot of new stuff right here! Good luck for the next!